1. Executive Summary

The United States faces a structural vulnerability in the supply of heavy rare earth elements (HREEs)—particularly dysprosium (Dy), terbium (Tb), and yttrium (Y)—which are essential to defense systems, permanent magnets, and advanced industrial applications. Despite increasing focus, the U.S. remains fully import dependent for these materials, with foreign supply chains that are exposed to geopolitical disruption, price volatility, and export controls.

Over the past decade, numerous domestic rare earth projects have been proposed, often emphasizing favorable geology, large resource estimates, or promising laboratory results. Yet very few have progressed to permitted, operating, and economically viable production, especially when it comes to HREEs. This gap reflects a fundamental reality: resources alone do not create supply. In practice, deployment constraints—permitting timelines, capital intensity, scalability, and cost—determine whether a project can translate into real supply.

This white paper introduces a deployment-focused screening framework designed to identify domestic HREE pathways that can realistically be financed, built, and scaled. Rather than ranking projects by theoretical resource size or early-stage technical promise, the framework applies five practical criteria that directly affect time to revenue, capital efficiency, and risk:

1. Domestic – Feedstocks and processing must be physically located in the United States and not reliant on foreign intermediates.

2. Permittable – Projects must fit within existing federal and state regulatory frameworks, avoiding long-duration greenfield mining approvals.

3. Timing – Pathways must deliver HREEs on timelines relevant to near-term defense and industrial demand.

4. Modular Deployment – Capital must be deployable incrementally through repeatable, scalable units rather than a single, high-risk megaproject.

5. Cost – Solutions must be competitive on a fully loaded basis, particularly for HREEs.

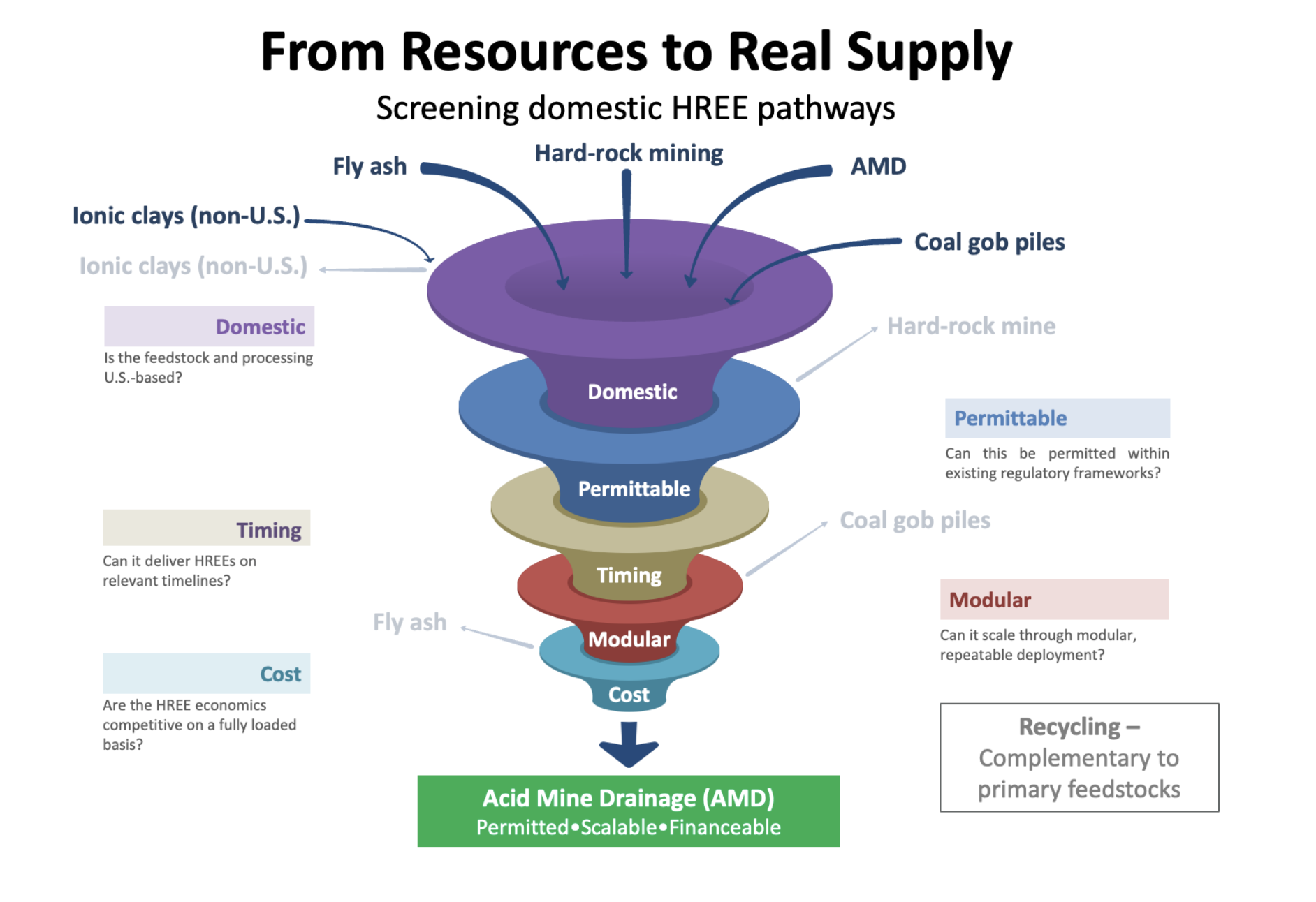

Applied sequentially, this framework rapidly narrows the universe of commonly cited domestic solutions. Conventional hard-rock mining projects often fail due to permitting duration, capital intensity, or unfavorable HREE economics. Other feedstocks, such as fly ash or coal gob piles, demonstrate conditional, site-specific potential but lack the consistency required for scalable national deployment. Ionic clay deposits, while heavy-rich and cost-advantaged, fail the foundational requirement of domestic control.

Only a narrow set of pathways pass all five criteria. Among them, acid mine drainage (AMD)—a legacy environmental liability already subject to mandatory treatment—emerges as a uniquely aligned feedstock. AMD supports domestic sourcing, accelerated deployment, modular scaling, competitive HREE economics, and environmental remediation.

The purpose of this paper is not to promote a single project, but to provide clarity and discipline in how domestic HREE opportunities are evaluated. By shifting the discussion from “what exists” to “what can be deployed,” this framework offers investors, policymakers, and industry leaders a practical lens for prioritizing solutions capable of delivering real supply within the timeframes that matter most.

1. Why Screening Matters

Discussions of domestic rare earth supply frequently focus on what resources exist rather than what can be deployed. In practice, supply chains are defined not by geology, but by permitting timelines, capital requirements, scalability, and cost. The failure to distinguish between these realities has been a recurring weakness in U.S. rare earth development efforts.

Over the past decade, many domestic projects have been announced with compelling resource estimates or promising laboratory results. Yet very few have progressed to permitted, operating, and economically viable production, particularly for HREEs. This outcome reflects a lack of deployment-focused screening rather than a lack of technical ideas.

Resource size alone is a poor predictor of deployable supply. Projects with large in-ground resources can still fail due to prolonged permitting, high upfront capital intensity, low HREE contents or yields, or extended timelines to cash flow. For investors and policymakers alike, these constraints matter more than headline tonnage.

The challenge is especially acute for HREEs. Many projects that appear attractive on a total rare earth oxide basis ultimately underperform when evaluated on HREE economics, leading to margin pressure and capital strain. As a result, broad claims of “domestic rare earth supply” often obscure whether a pathway can deliver Dy, Tb, and Y in meaningful quantities and on relevant timelines.

Screening provides a disciplined way to narrow a wide universe of theoretical opportunities into a small set of deployable pathways. The framework presented in this paper focuses on execution rather than aspiration, enabling clearer prioritization of projects capable of

producing real supply.

2. The Five-Criteria Screening Framework

The screening framework applies five sequential criteria that reflect how projects are financed, permitted, and built in practice. These criteria function as gates rather than weighted factors; reflecting the reality that failure at any stage prevents practical deployment.

• Domestic – Feedstocks and processing pathways must be physically located in the U.S. and not dependent on foreign intermediates. Domestic control reduces geopolitical risk, pricing volatility, and supply disruption, and is foundational to both national security and investment certainty.

• Permittable – Projects must fit within existing federal and state regulatory frameworks. Pathways requiring long-duration greenfield mining permits or extensive land disturbance introduce delays and uncertainty that are difficult to finance and rarely compressible.

• Timing – Projects must be capable of delivering HREEs within a timeframe aligned with near-term defense and industrial demand. Extended development timelines increase capital exposure and reduce risk-adjusted returns, even if projects eventually succeed.

• Modular Deployment – Capital should be deployable in repeatable, scalable modules rather than as a single, irreversible investment. Modularity enables staged capital deployment, faster ramp-up, and reduced execution risk, while supporting distributed feedstocks and system resilience.

• Cost – Solutions must be competitive on a fully loaded basis, particularly for HREEs. Many projects appear viable on total output but underperform due to low HREE yield or high processing intensity. Sustainable supply requires cost structures aligned with HREE value.

Applied sequentially, these criteria quickly narrow the field to pathways capable of producing deployable, scalable supply rather than theoretical capacity.

3. Applying the Framework

Applying the framework highlights clear differences among commonly cited rare earth feedstocks.

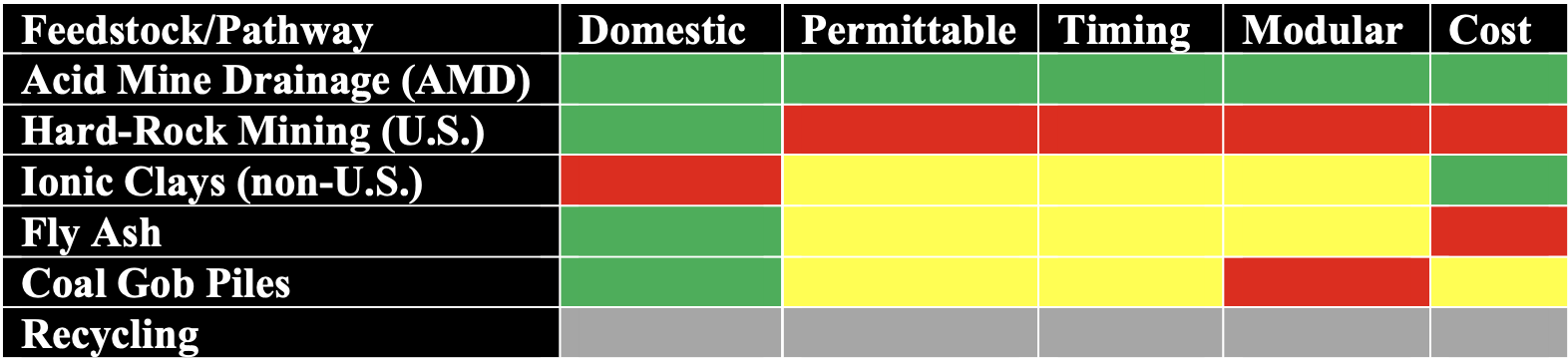

• Acid Mine Drainage (AMD) uniquely passes all five criteria. AMD is a domestic, mandatory-treated environmental liability that can often be integrated into existing permitted infrastructure. Deployment timelines are short, systems are modular and repeatable, and the absence of mining and primary leaching steps supports favorable heavy rare earth economics. AMD aligns environmental remediation with material recovery, reducing both permitting complexity and capital intensity.

• Conventional Hard-Rock Mining (Domestic) satisfies domestic sourcing but fails multiple deployment criteria. Greenfield permitting timelines are long and uncertain, capital requirements are large and front-loaded, and HREE yields are often low. While such projects may contribute to long-term supply, they are poorly suited to near-term HREE delivery.

• Ionic Clays (non-U.S.) offer favorable HREE chemistry but fail the foundational domestic criterion. Dependence on foreign feedstocks and processing introduces geopolitical and supply-chain risk incompatible with a domestically controlled strategy.

• Fly Ash and Industrial Residues are domestic and potentially permittable but highly variable. Differences in composition, recovery performance, and site-specific permitting limit standardization and scalability. These materials may support selective recovery efforts but lack consistency as a national solution.

• Coal Gob Piles are often grouped with AMD but differ materially in practice. Recovery typically requires new excavation, material handling, and site-specific permitting. Variability in composition and higher processing costs limit repeatability, making gob piles opportunistic rather than broadly scalable.

Recycling is intentionally treated outside the primary feedstock screening framework. Recycling does not create new primary HREE supply; it recovers material that has already in circulation. In addition, bulk recycling streams—particularly permanent magnets—are typically dominated by light rare earth elements and contain comparatively low and variable HREE concentrations. As a result, recycling is best positioned as a complementary input, enhancing utilization and resilience of domestic processing infrastructure rather than serving as a primary source of HREE supply.

Overall, only a narrow set of pathways—led by AMD—align domestic control, permitting reality, near-term timing, modular deployment, and competitive HREE economics. The screening outcomes discussed above are summarized in Figure 1 below.

4. Strategic Implications and Conclusions

As illustrated by the screening framework, only a narrow set of pathways align with the permitting, timing, scalability, and cost requirements needed to deliver real supply. This outcome has important implications for capital allocation, policy prioritization, and domestic supply chain development.

For investors, the screening framework highlights opportunities with clearer paths to construction, staged capital deployment, and earlier cash flow—reducing exposure to stranded capital and prolonged dilution. For policymakers, it offers a disciplined tool to prioritize funding toward projects capable of delivering near-term supply rather than aspirational capacity.

From an industrial strategy perspective, deployable feedstocks can anchor domestic processing infrastructure, enabling downstream integration and future incorporation of recycling and secondary streams. This system-level approach favors modular growth, infrastructure reuse, and resilience.

Success in U.S. heavy rare earths will belong to projects that can be deployed, not merely proposed. Applying disciplined screening enables investors and policymakers to prioritize pathways capable of producing real supply within relevant timeframes.

Appendix A — Heat Map of Domestic HREE Pathways

Purpose: The heat map shown in the table below provides a side-by-side application of the five screening criteria to commonly cited HREE pathways. It is intended as a validation tool that reinforces the sequential funnel outcome, not as a scoring or ranking exercise.